Super apps are widely used in other countries, yet there’s still no super app ecosystem available in the U.S. or Europe, primarily due to regulatory concerns about the risks associated with these all-in-one app platforms.

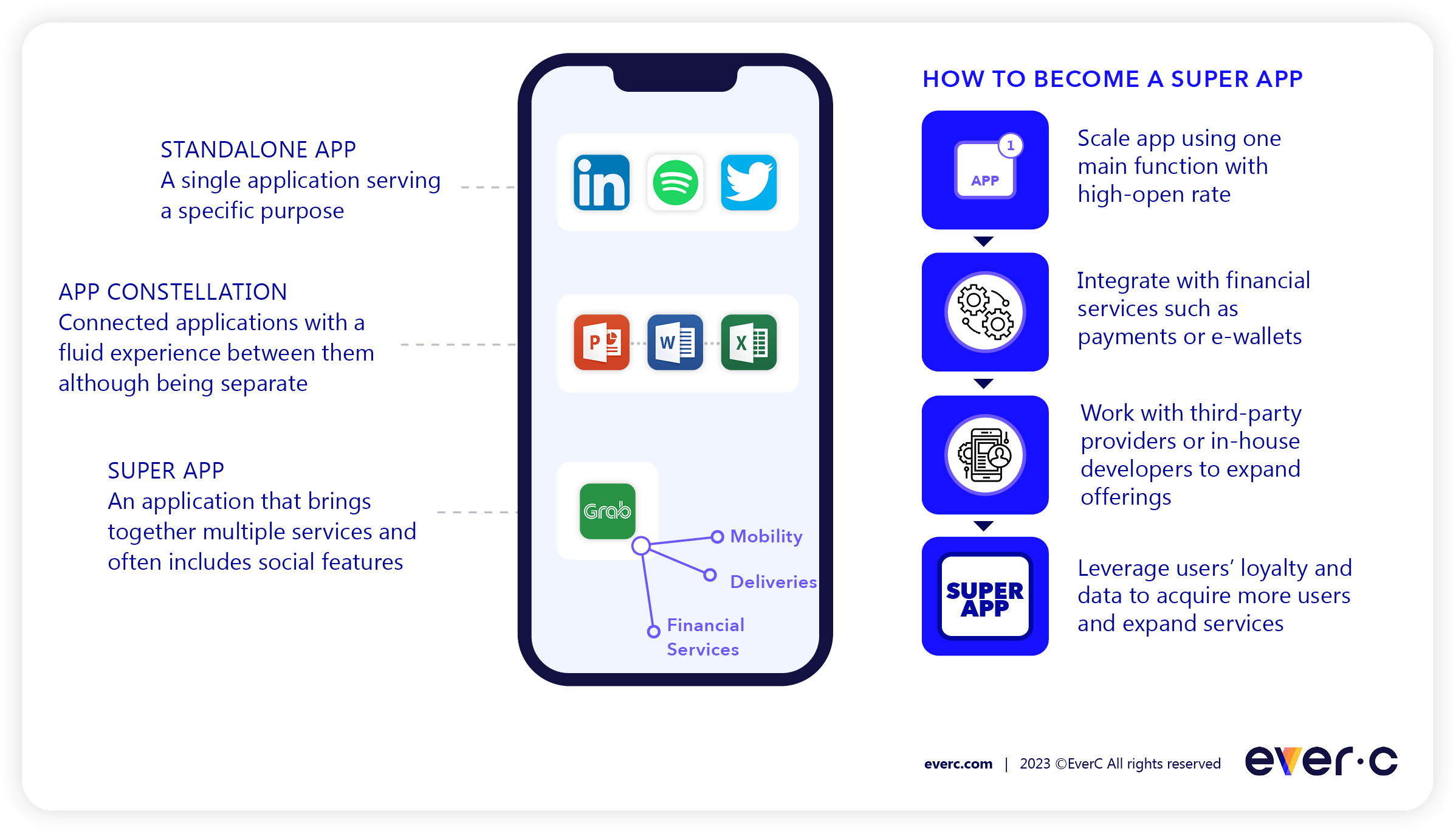

What is a super app?

A super app is an app ecosystem that provides multiple services all in one place, creating a one-stop shop for consumers. Super apps enable users to manage many day-to-day tasks all in one place on their smartphone. At the same time, they enable companies to rapidly scale and expand their services while lowering development costs – a process which is often supported by partnerships and third-party providers.

The evolution of super apps

Super apps aren’t new. The first company to successfully implement the concept was WeChat, a Chinese instant messaging, social media, and mobile payment app developed by Tencent.

Super apps have since become the standard across Asia, Latin America, and Africa. Alipay rivals WeChat, with its vast user base in China. Grab is the leading super app across southeast Asia. Mercado Libre and Rappi have a sizable hold on the Latin American market. Super apps have even gained popularity in African countries like Kenya and Egypt. Smartphones in many of these areas don’t have the horsepower capable of hosting dozens of separate apps, which has been a driver of super app demand.

In the West, a recent survey showed 72% of consumers are interested in super apps, with tech giants already in the race to dominate the U.S. market share. For instance, Elon Musk tweeted last year that the purchase of Twitter was just the next step in creating X, the everything app. PayPal and Walmart have also been teasing their own versions since 2021, and even Microsoft is considering building its own platform

Regulatory concern over privacy leaks from super apps

Regulators are concerned that super app companies will gather an extensive amount of personal and sensitive user information – data that could potentially be abused for commercial and advertising purposes, or worse. That’s why consumer protection laws remain at the forefront in places like the EU to restrict sharing, selling, and leveraging user data for corporate gain.

Officials in the US have taken similar steps in recent years. For instance, the Federal Trade Commission (FTC) has put companies developing health apps “on notice” out of concern that consumers’ sensitive information could be used or shared with advertisers or other third parties.

Why super apps pose greater risk

As an application expands across industries, including new API endpoints, pages, and users, it creates a larger attack surface for cybercriminals to infiltrate. The sheer complexity of super apps makes it easier for bad actors to locate security oversights and harder for administrators to monitor potential attacks.

This becomes especially risky as super apps are expected to disrupt the banking sector over the coming years. What's more, there is a high incentive for developers to rush to make new offerings and mobile features available, often at the expense of comprehensive security protocols.

Indeed, users and merchants partnering with super app platforms are subject to an increased level of risk. If there is a data breach, consumers using several different apps need to worry about a criminal accessing their information from only one or two places. If a breach occurs on a super app, criminals could gain access to a wide range of consumer data stored across the platform's ecosystem.

The rise of the super app will likely result in rising risks for consumers and payment providers alike. Want to learn more?