The fate of the Consumer Financial Protection Bureau (CFPB) is now in question, but the regulatory agency seems to have foreseen that its future would be uncertain under the new administration. The bureau, which began operating in 2011 after the financial crisis, preeminently issued guidance early this year on how its work might continue in the event of a federal regulatory shift, urging states to take the lead in consumer protection.

How will all of this affect the payments industry? We don’t have all the answers, but we believe it’s bound to make compliance even more burdensome and complex than it already is. Let’s take a look at the recommendations the CFPB has passed down in its new report.

What Guidance Has the CFPB Issued for States?

In January, the CFPB released a new report titled “Strengthening State-Level Consumer Protections: Promoting Consumer Protection Federalism.” The report acknowledges that consumer protection law has often been the result of state-federal partnership, in which “states have often taken the lead.”

According to the report, “federal law should be a floor, not a ceiling, for the protection of consumers.” It goes on to say that with the passage of the Dodd-Frank Act, also known as the Consumer Financial Protection Act (CFPA) of 2010, “Congress intended federal law to establish ‘minimal standards’ for consumer protection,” and that state laws should be able to provide more protective standards for consumers beyond federal law. The CFPB was created under this legislation.

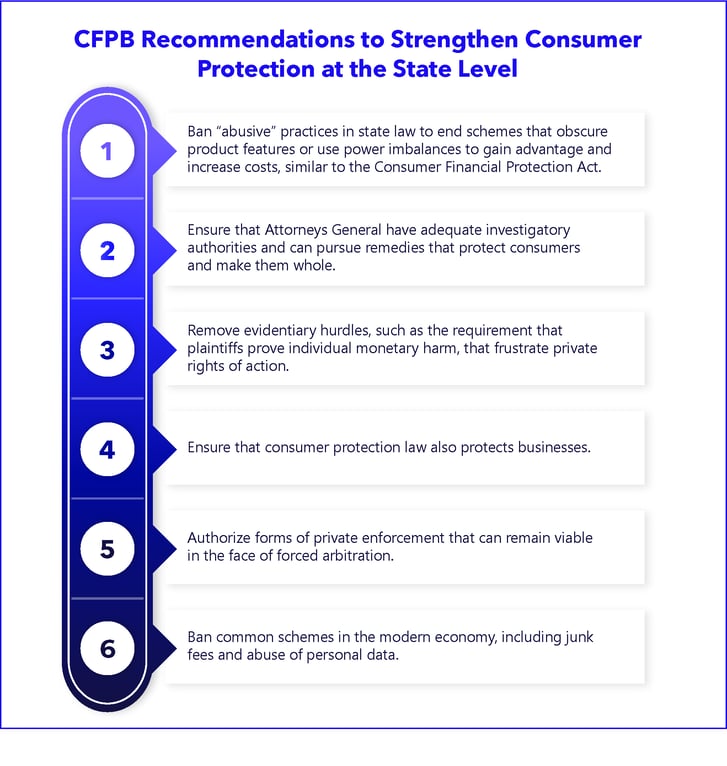

The report outlines a roadmap of sorts, encouraging states to “modernize the standards of fair dealing using models already existing in state or federal law” through a number of measures, which are laid out in the executive summary:

What Happens Next?

Only time will tell what will happen if the CFPB is permanently shuttered. However, we can confidently predict risk mitigation in the payments industry would inevitably become much more burdensome and complex than it already is. Instead of one overarching agency to answer to, financial institutions and payment providers conducting business nationally or globally would have to manage compliance with regulations from all 50 states, each with their own approaches to oversight and risk.

How can we help?

Our unique combination of expertise, data, and technology helps marketplaces, payment providers, acquirers, and banks to mitigate risk while enhancing operational efficiency so they can focus on revenue and growth. If you’re looking for help navigating the complexities of compliance, talk to us.